How to Use a Personal Loan for Debt Consolidation

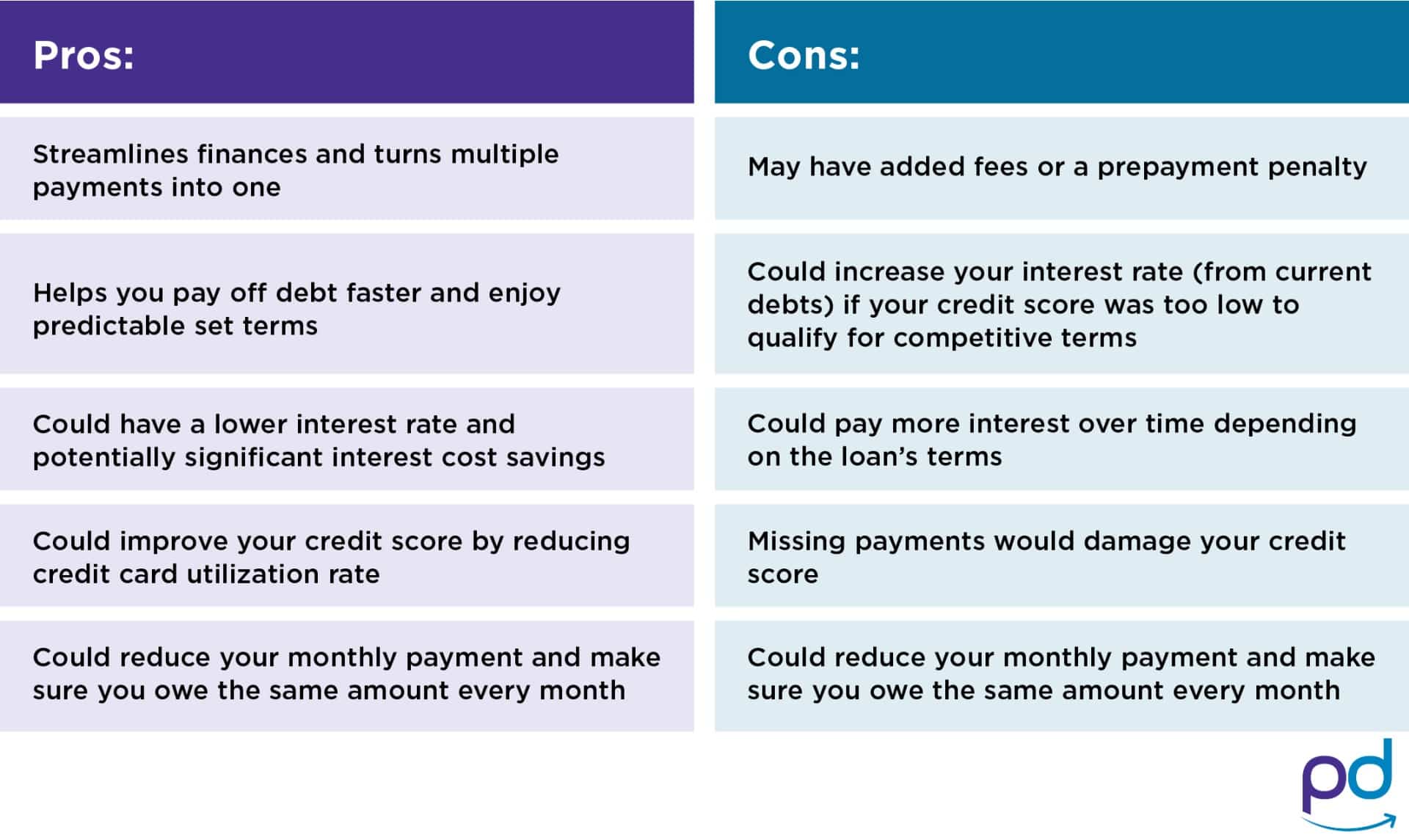

Making minimum payments on high-interest credit card debt is an exhausting way to manage your finances. You are paying every month, but the balance barely moves because most of what you pay goes straight to interest. A personal loan for debt consolidation may offer a way out. By replacing multiple high-rate balances with one fixed-rate loan at a lower rate, you can reduce your monthly payment, pay less interest over time, and see a clear finish line on your debt.

A personal loan from People Driven Credit Union gives you access to loan consolidation experts who can help you evaluate whether this approach makes sense for your situation and guide you through the process.

What Is Debt Consolidation?

Debt consolidation means using the funds from one loan to pay off several other debts, typically high-interest credit cards or other unsecured balances. You are trading multiple debt obligations for a single one, usually with a lower interest rate, a fixed monthly payment, and a defined payoff date.

Personal loans used for debt consolidation can be unsecured, meaning no collateral is required, or secured, meaning you put up an asset like a vehicle or savings account to back the loan. Unsecured personal loans are the most common choice for credit card consolidation. Your approval and rate depend primarily on your credit score and income.

Pros and Cons of Debt Consolidation

When Does a Debt Consolidation Loan Make Sense?

Debt consolidation is a tool that works well under the right conditions. It is worth considering if you meet most of the following:

You have a meaningful amount of high-interest debt, typically several thousand dollars or more across multiple accounts.

Your credit score is high enough to qualify for a rate lower than what you are currently paying on your cards. A score above 700 gives you the best odds of approval at a competitive rate, though credit unions like PDCU are more willing than banks to consider your broader financial picture.

You can comfortably manage the monthly loan payment, which may be higher than your current minimum payments if you have been paying minimums for a long time.

You are committed to not adding new credit card debt while repaying the loan. Consolidation helps you get out of debt. It does not help if the same spending habits that created the debt continue.

If your debt is small, your credit score makes qualifying for a lower rate unlikely, or the underlying financial habits that created the debt have not changed, consolidation may not deliver the results you are hoping for.

How to Apply for a loan for Debt Consolidation Loan

Step 1: Assess Your Finances

List every debt you carry, the balance, the interest rate, and the minimum monthly payment. Add them up. Calculate your debt-to-income ratio by dividing your total monthly debt payments by your gross monthly income. A ratio below 45 percent generally gives you a reasonable chance of qualifying for a personal loan. This exercise also helps you determine how much you need to borrow and what monthly payment you can realistically afford.

Step 2: Check Your Credit Score

PDCU members can check their credit score and use the score simulator for free inside the MyPDCU app. You can also request free credit reports from all three major bureaus annually at AnnualCreditReport.com. Review your report for errors before you apply since an incorrect negative item could be lowering your score unnecessarily.

Step 3: Compare Lenders

Not all lenders are equal. Some charge origination fees, prepayment penalties, or high rates that offset the benefit of consolidating. Compare interest rates, fees, loan terms, and how quickly you can receive funds. If your credit score is less than ideal, a not-for-profit credit union like PDCU is more likely to evaluate your full financial picture rather than relying solely on a number.

Step 4: Apply to use a personal Loan for debt consolidation

Gather the documents most lenders require before you apply. This typically includes proof of identity such as a driver’s license, proof of address such as a utility bill or bank statement, and proof of income such as recent pay stubs, W-2s, or tax returns. Having these ready speeds up the process significantly.

Step 5: Close the Loan and Pay Off Your Balances

Once approved, sign the loan documents and receive your funds. Pay off the balances you are consolidating immediately. Do not keep those credit card accounts running with new charges. Your goal is a single fixed monthly loan payment replacing the multiple minimum payments you were juggling before.

Tips for Getting Your Finances in Order After Consolidation

A debt consolidation loan is a fresh start, not a blank check. Here are five habits that make the difference between getting out of debt and ending up back in it.

Budget every month. Track every purchase. Whether you use an app, a spreadsheet, or pen and paper, recording your spending keeps you aware of where your money is going before it is gone.

Automate your payments. Set up AutoPay on your PDCU loan and anywhere else you can. Missing a payment damages your credit score and adds fees. Automation eliminates that risk entirely.

Consolidate accounts where possible. Multiple checking accounts, old 401k accounts from previous employers, and scattered savings accounts create unnecessary complexity. Simplify your financial life so you can see the full picture clearly.

Address your income if needed. If your expenses genuinely exceed your income, no amount of loan restructuring solves the problem permanently. Consider whether a higher-paying role, additional hours, or a side income is realistic in your situation.

Close credit cards you do not need. After paying off a card with your consolidation loan, consider closing it if you do not need it. Fewer open revolving accounts reduces the temptation to add new debt.

Ready to Get Started?

People Driven Credit Union personal loans for debt consolidation come with competitive rates, no prepayment penalties, and an application that takes minutes. You could have funds in as little as a few days. Apply online today or talk to one of our loan experts to find out what you qualify for.

Ready to Replace Multiple Payments with One?

A PDCU personal loan for debt consolidation gives you a fixed rate, a predictable payment, and no prepayment penalty. Here are three ways to take the next step today.

Apply for a Personal Loan

Apply online in minutes. Competitive fixed rates, flexible terms, no prepayment penalties, and funds available in as little as a few days for eligible members. All loans subject to credit approval and membership eligibility.

Talk to GreenPath Financial Wellness

Not sure if consolidation is the right move for your situation? GreenPath Financial Wellness offers free confidential debt counseling for PDCU members. Call 877-337-3399 to build a plan at no cost before you apply.

Check Your Credit Score First

PDCU members can check their credit score and use the score simulator inside the MyPDCU app to see how paying down balances might improve their rate before they apply. Free for all members with no impact to your score.

All loans subject to credit approval and membership eligibility. Rates and terms vary based on individual creditworthiness. GreenPath Financial Wellness is a nonprofit organization. Services available to PDCU members at no cost. Federally insured by the NCUA. Equal Housing Lender. NMLS #776727.How to use a personal Loan for debt consolidation

Dave Sullivan is Vice President of Marketing, Sales and Service at People Driven Credit Union, where he helps guide member communications, financial education, and digital growth. With a background in credit education, lending, and member service, Dave focuses on making financial topics easier to understand and more useful in everyday life. His work helps connect members with practical information, helpful resources, and financial solutions that support their goals.

View More Posts